Why is there a conflict between my Absolute Return and Return in Percentage?

Why is there a conflict between my Absolute Return and Return in Percentage?

Time-Weighted Return (TWR) vs Absolute Return

Time-Weighted Return (TWR)

To calculate return as a percentage, Totality Capital Markets applies the industry-standard TWR methodology.

- TWR is calculated as the compounded return of daily returns over the evaluation period (e.g., 1 year).

- This approach ensures returns are measured independently of cash inflows and outflows, making it a common metric for assessing investment performance.

Absolute Return

Absolute Return measures performance by comparing the Account Value at time (t+1) vs Account Value at time (t), while adjusting for:

- Account funding (deposits)

- Account withdrawals

Potential Conflict Between TWR and Absolute Return

TWR does not consider portfolio size when calculating sub-period returns:

- If sub-periods with low account value show high positive returns, while sub-periods with high account value experience slightly negative returns, the total TWR may still be positive.

- However, the Absolute Return over the same period could be negative, leading to a discrepancy between the two metrics.

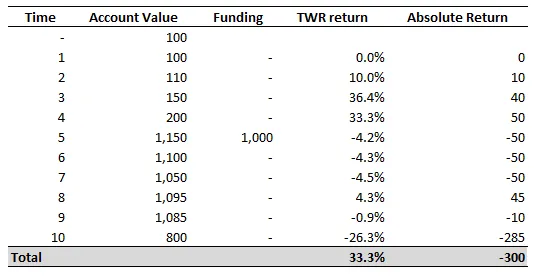

Illustrative Example

In the following case, the TWR is positive (+33%), but the Absolute Return is negative (-300) due to fluctuations in portfolio size and cash movements.

Would you like further insights or a more detailed breakdown of how TWR compares to Absolute Return in practical investment scenarios?

Take total control of your portfolio, today.

Trade smarter with Totality - formerly Saxo Australia. Join 1,000s of investors building global portfolios with low fees, local support, and world-class platforms.

Institutional-grade trading infrastructure powered by Saxo

Totality platforms are built on Saxo’s global trading infrastructure, providing deep liquidity, robust execution, and enterprise-level reliability trusted by financial institutions worldwide.

Totality is the Official Online Trading Partner of Sydney's Allianz Stadium

From bespoke matchday experiences to unrivalled networking opportunities, our partnership with Allianz Stadium puts Totality clients at the heart of the action.