What are FX Rollovers?

FX spot trades through the Totality platform do not settle. Instead, open positions held at the end of a trading day (1700 EST) are usually rolled forward to the next available business day. In such a case, the opening price is adjusted.

This rollover is made up of two components: the Tom/Next swap points (Forward Price), and the financing of unrealised profits/losses (Financing Interest).

Rollover Methodology for retail clients:

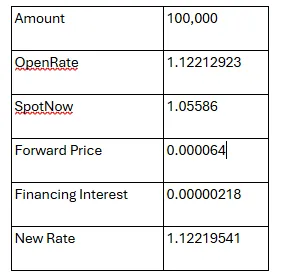

Normal Forward (price adjustment to the opening price of a position). An example:

The rollover is applied by:

- Adjusting the opening price of a position to include the Forward Price and Financing Interest components:

- OpenRate + Forward Price + Financing Interest = New Rate

- 1.12212923 + 0.000064 + 0.00000218 = 1.12219541

- No closing rate and no closing position is generated for a swap executed using this method.

Totality publishes for full transparency the historic swap points used for the Tom/Next rollover on a daily basis.

You can view the rollover history on your FX positions via the Totality platform.

Year-end ‘turn’ effect in FX swap points:

The “turn” effect is a phenomenon that exists in financial markets which is caused by supply and demand for funding over key dates, such as year or quarter-end. This can create anomalies in the forward curves for certain currencies, which may be priced into the year-end swap points that we receive from our liquidity providers.

Swap points are a key component of the FX Value Date Rollover, which is used to adjust the opening price of a position (applicable to the default rollover methodology). Therefore, if you hold a FX spot position over year-end, you may bear the cost of paying these inflated swap points (depending on the currency pair) when compared to normal market conditions.

Take total control of your portfolio, today.

Trade smarter with Totality - formerly Saxo Australia. Join 1,000s of investors building global portfolios with low fees, local support, and world-class platforms.

Institutional-grade trading infrastructure powered by Saxo

Totality platforms are built on Saxo’s global trading infrastructure, providing deep liquidity, robust execution, and enterprise-level reliability trusted by financial institutions worldwide.

Totality is the Official Online Trading Partner of Sydney's Allianz Stadium

From bespoke matchday experiences to unrivalled networking opportunities, our partnership with Allianz Stadium puts Totality clients at the heart of the action.